RIP CURL Phantoms from SD Eyes

Photographed by Ned Matura

Moving onward from the challenges encountered in recent years, the sunwear market makes a vital comeback. 20/20 presents our annual Sunwear MarketPulse Survey 2022 conducted by Jobson Research, surveying independent optical retailers on their sunwear sales performance and emerging market trends. Sunwear continues to be a favorite accessory among consumers, and with its growth trending again in a positive direction, the future looks bright.

–Jennifer Waller, 20/20 Director of Research & Business Analytics

- Sixty-six percent of respondents said that Rx sunwear is growing for their practice. This is up significantly from a dramatic dip last year likely due to the Covid-19 pandemic.

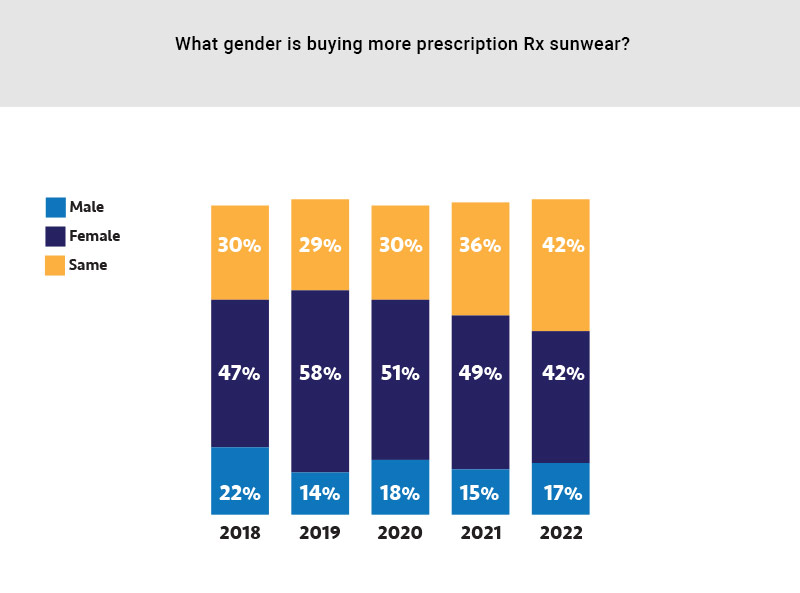

- Adults (ages 35 to 44) accounted for the largest percent of Rx sunwear sales (an average of 31 percent) according to those independents surveyed. Forty-two percent of respondents said that females are buying more Rx sunwear than males. Seventeen percent said males more than females, and 42 percent said the same for both genders.

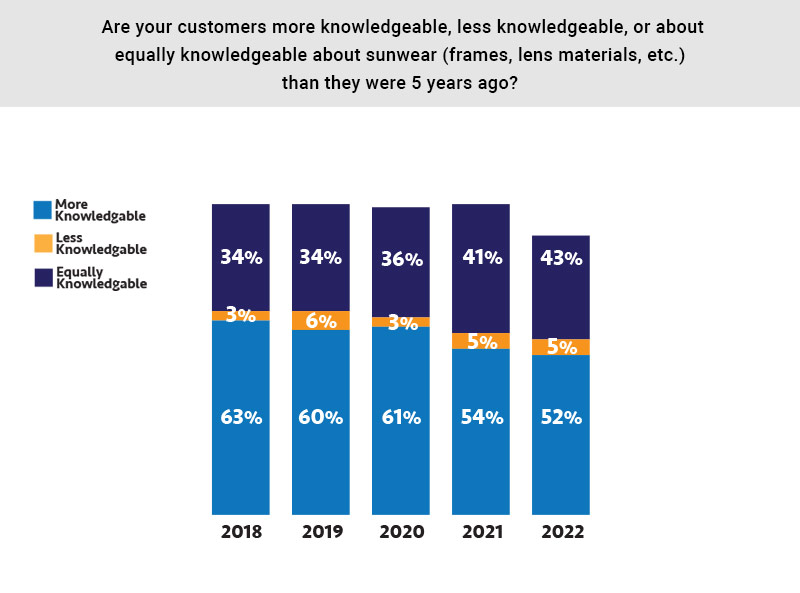

- Of the independents surveyed, 52 percent said consumers are more knowledgeable about sunwear than they were five years ago.

- Forty-two percent disagreed with the statement that they feel the lines between fashion oriented sunwear and sports oriented sunwear are blurring compared to 43 percent agreeing (16 percent said don’t know). Of the 43 percent who agreed that the lines are blurring, 39 percent think this is helping the sales of both Rx and plano sunglasses. Only 7 percent claim the merging is hurting their sunwear sales.

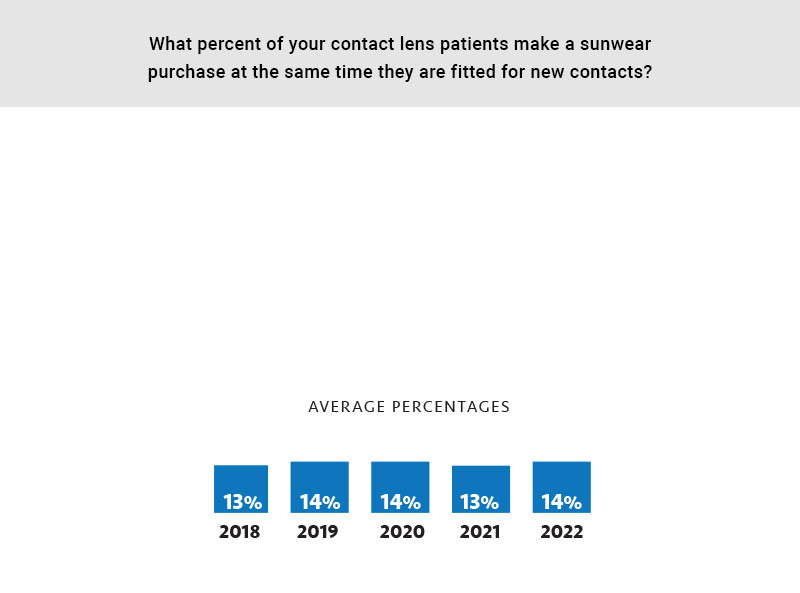

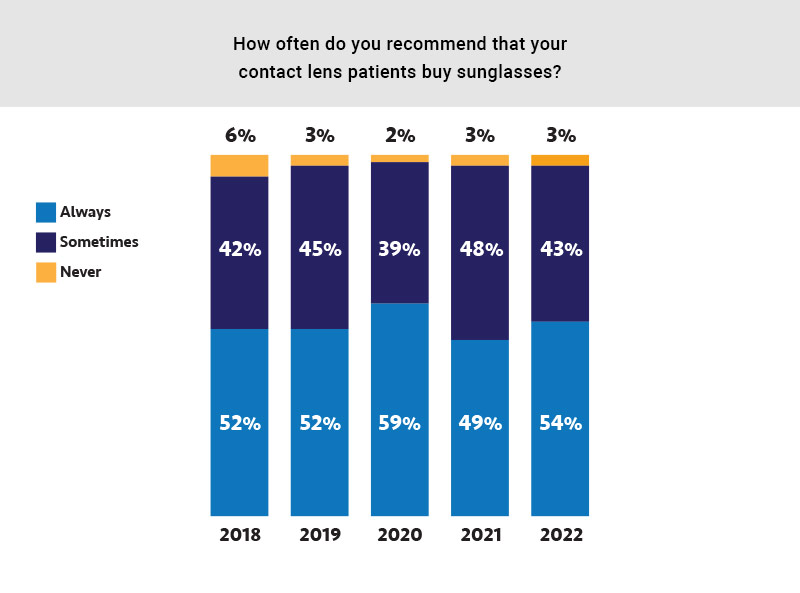

- Over half (54 percent) of independents surveyed said they always recommend that their contact lens patients buy sunglasses. However, respondents said only 14 percent of their patients, on average, actually make a sunwear purchase at the time they are fitted for new contacts.

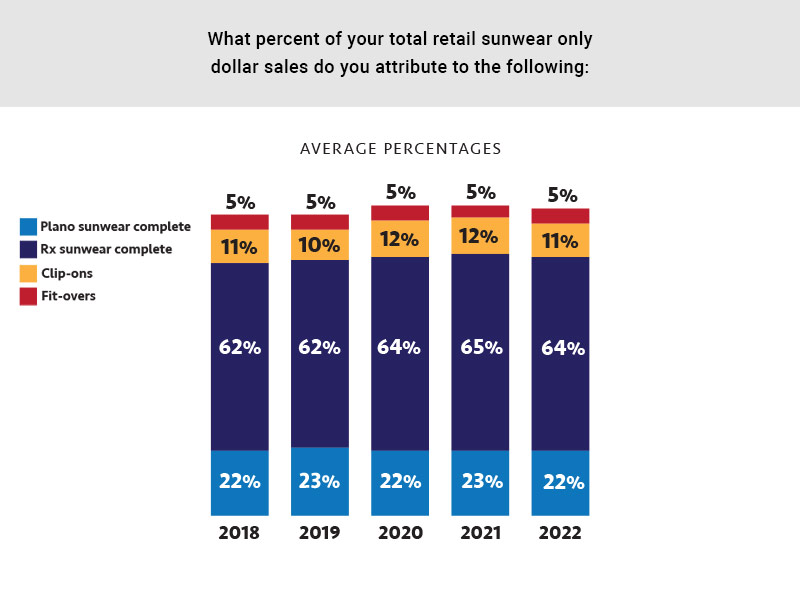

- On average, respondents said 64 percent of total retail sunwear comes from Rx complete, 22 percent from plano complete, 11 percent from clip-ons and 6 percent from fit-overs.

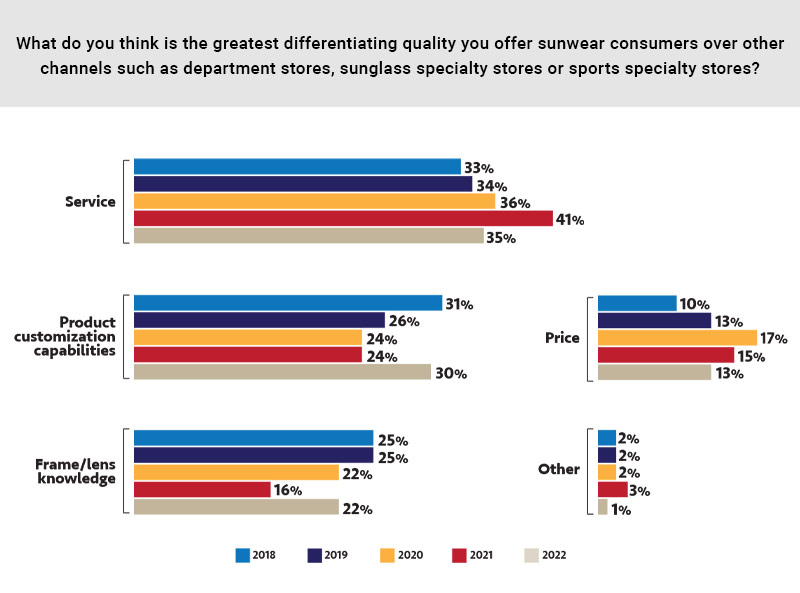

- When asked what the greatest differentiating quality independents have over other channels was, superior service takes the top spot with 35 percent, followed by product customization at 30 percent and frames/lens knowledge at 22 percent.

- On average, independents said polycarbonate lenses made up 45 percent of their total prescription sun lens sales and 44 percent of plano sunwear lens sales as well. Plastic/high-index plastic lenses made up 49 percent of total prescription sun lens sales and 53 percent of plano sunwear lens sales.

- Not surprisingly, July/August was rated the highest sunglass sales period for 65 percent of independents. May/June followed with 54 percent rating it as a “high” period for sunglass sales. For comparison, January/February came in only at 3 percent rating it high.

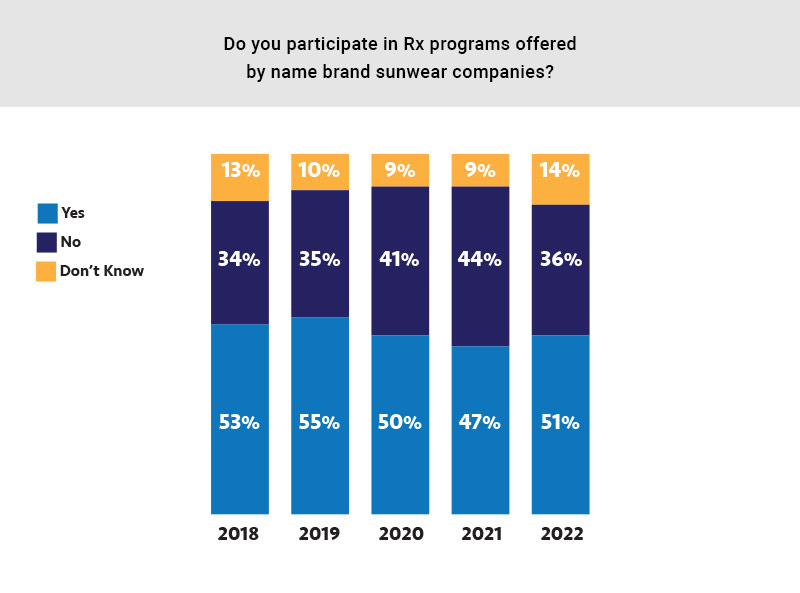

- Just over half of independents say they participate in Rx programs offered by sunwear companies (51 percent). Fourteen percent were unsure.

Source: 20/20’s Sunwear MarketPulse Survey

Source: 20/20’s Sunwear MarketPulse Survey

Source: 20/20’s Sunwear MarketPulse Survey

Source: 20/20’s Sunwear MarketPulse Survey

Source: 20/20’s Sunwear MarketPulse Survey

Source: 20/20’s Sunwear MarketPulse Survey

Source: 20/20’s Sunwear MarketPulse Survey

Source: 20/20’s Sunwear MarketPulse Survey

Source: 20/20’s Sunwear MarketPulse Survey

Source: 20/20’s Sunwear MarketPulse Survey

Source: 20/20’s Sunwear MarketPulse Survey

Source: 20/20’s Sunwear MarketPulse Survey

METHODOLOGY

20/20's Sunwear MarketPulse Survey 2022 is based on data collected from structured e-mail interviews with 166 independent optical retailers. The samples were derived from the proprietary Jobson Database. All 2022 interviews were conducted in May 2022. This study is conducted annually. Trended data is charted wherever possible. All participants were contacted via e-mail invitation and offered an incentive of a chance to win a $200 amazon.com gift card. For more information, contact [email protected] or (212) 274-7164.

![]()