feedback from eyecare practitioners about sales of the spectacle lens designs, materials and treatments

they prescribe and dispense. By analyzing the results of this new study, which polled 166 independent

optical retailers across the country, we learn which products they think are hot and which ones are

not compared with last year. Use this field data to benchmark your own lens sales. —Andrew Karp

TOTAL SALES

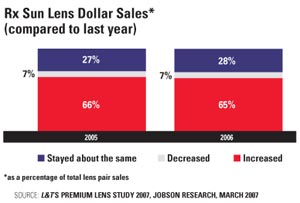

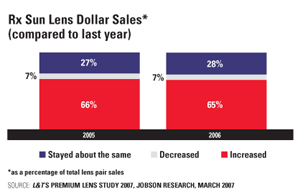

Compared to three years ago, 72 percent of retailers said that in 2006, spectacle lenses and treatments made up a larger percentage of their location’s total gross dollar sales. This is down, however from 76 percent last year. There was also a slight decrease in the number of retailers who said spectacle lenses and treatments made up a smaller percentage compared to three years ago, going from 9 percent in 2005 to 8 percent in 2006. Sixtyfive percent said Rx sun lenses as a percentage of total dollar sales increased over three years ago.

LENS SALES

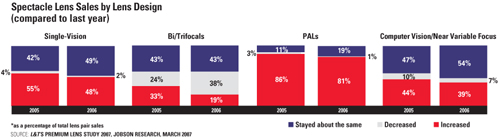

When asked to rank lens design by popularity, single vision was ranked number one by over half (52 percent) of retailers. Progressive (including short corridor) was ranked number one by 42 percent.

Almost half (48 percent) of retailers said single-vision lenses made up a greater proportion of their total lens sales in 2006 than they had in 2005. Comparatively, 81 percent said progressive sales had increased, while 38 percent said sales of bifocals and trifocals had decreased as a percentage of total lens sales.

Seventy-four percent of retailers agree with the statement, “I promote the use of progressive lenses to all my presbyopic patients, including those who currently wear bifocals or trifocals.”

COMPUTER/OFFICE LENSES

Computer vision sales have stayed about level, with 54 percent of retailers saying their sales in this area have remained unchanged. Most retailers surveyed (74 percent) said computer/office lenses make up an insignificant percentage (10 percent or less) of their total lens pair sales.

SHORT CORRIDOR PALS

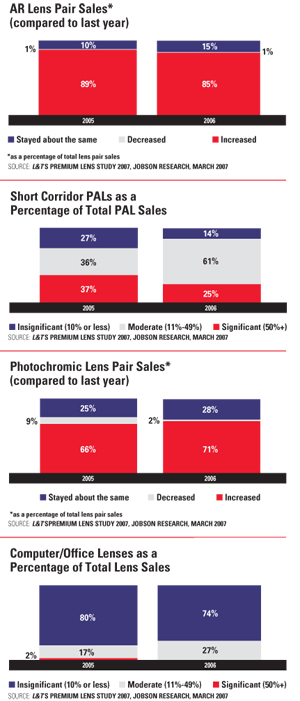

Twenty-five percent of retailers said short corridor lenses were a significant percentage (50+ percent) of their progressive lens pair (PAL) sales. This is down, however, from 37 percent last year. Eighty-nine percent of retailers said they offer more than one short corridor progressive lens design and 83 percent claim they dispense a higher number of these lenses to females than males.

LENS MATERIALS

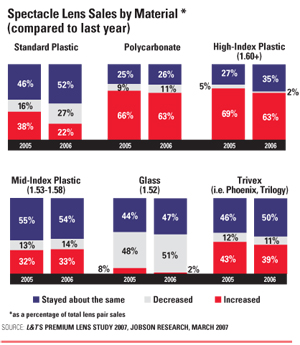

When asked to rank lens material by popularity, standard plastic was ranked one by almost half (47 percent) of retailers. Polycarbonate was ranked one by 38 percent. Glass was ranked least popular by the most retailers (63 percent).

Fifty-two percent of retailers said their 2006 standard plastic lens sales stayed about the same as a proportion of total lens pair sales compared to 2005. Fiftyfour percent also said their midindex lens sales had stayed flat, while 50 percent said Trivex sales had remained the same. Sixty-three percent said their sales of polycarbonate lenses and high-index lenses had grown this year. Glass was the worst performer, with 51 percent responding glass made up a smaller proportion of their total lens sales in 2006 than in 2005.

HIGH-INDEX LENSES

When asked to rank high-index lenses based on popularity, 49 percent ranked 1.67 as most popular and 42 percent ranked 1.60 as most popular. Comparatively, 1.71 was ranked least popular by 66 percent of retailers.

LENS TREATMENTS

An impressive 85 percent of retailers surveyed said they had experienced an increase in AR lens sales as a proportion of total lens sales in 2006 vs. 2005. Seventy-two percent saw an increase in polarized lenses and 71 percent saw an increase in photochromic sales over the same period.

For 47 percent of retailers surveyed, tinted lens sales stayed about the same versus the year before. Sixty-nine percent of retailers said they offer two different price points for AR lenses— one being standard, the other being premium.

REFRACTIVE

SURGERY’S IMPACT

Ten percent of retailers agree that because of the increase in patients having refractive surgery, their overall lens sales have decreased. Twenty-five percent said specifically high-powered lens sales have decreased.

READING GLASSES

For most retailers (46 percent), reading glass sales stayed about the same in 2006 vs. the year before. Thirty-five percent of respondents experienced an increase in readers sales over this time period. Among those who sell readers, 58 percent said their OTC/ready-made readers sales had stayed flat in 2006. Custommade readers sales were also flat for 55 percent of respondents at locations that sell readers.

LENS AND LENS

TREATMENT PACKAGES

When asked about familiarity regarding new progressive lens technologies, three-fourths of respondents were aware of the term “digitally surfaced progressives.” Seventy percent are aware of the term “free form progressives” and 68 percent the term “personalized progressive.” This shows much more familiarity than last year when only 49 percent and 57 percent were familiar with the terms “free form progressive” and “personalized progressive,” respectively. The least familiar term is “direct surfaced progressives” (38 percent).

Forty percent of retailers said they do use lens-only package pricing. The average price of this lens-only package is $274.92.