From top: AIRMAG AF7028 from Clariti Eyewear; DAISY FUENTES Carolina from Zyloware; ADRIENNE VITTADINI 1910 from Match Eyewear

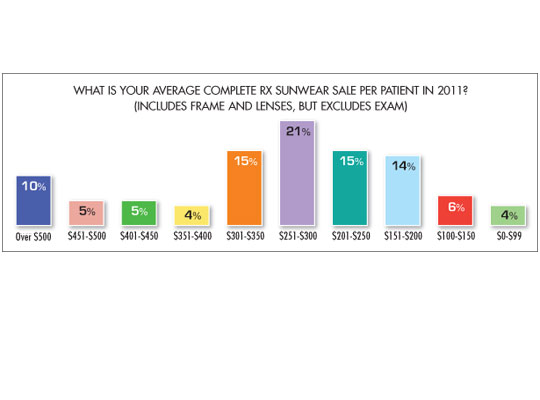

Photograph by Ned MaturaThe sunglass market continues to hold its own according to the findings of 20/20’s 2011 Sunwear MarketPulse Survey of independents conducted in October 2011. But the survey doesn’t point toward any striking overall changes in this segment of the market—undoubtedly because of lingering uncertainty about the economy. In fact, the percentage of participants who reported an increase in their sun business in the past year (66 percent) was almost the same as the 2010 figure (67 percent). Additionally in 2011 respondents said they expected sunwear products to account for only 9 percent of gross retail dollar sales for the year—again similar to the 8 percent cited in both 2009 and 2010. The average price for a complete pair of Rx sunwear per patient (including frame and lenses, but excluding the exam) is also holding steady. Current respondents cited the price as $318, just slightly less than the $326 reported in 2010. Moreover the vast majority of Rx sunglasses (75 percent) dispensed by the surveyed independents in the past year retailed on average for more than $200, and 20 percent sold for an average in excess of $400—again analogous to the 2010 figures of 79 percent and 19 percent, respectively.

SUNNY SIDE UP

Still a variety of statistics indicate sunwear remains a hot category with a great deal of future potential. Very importantly, consumers appear to be better informed about sunwear products than they were five years ago, according to 68 percent of the respondents. This number is up from 62 percent in 2010 and 58 percent in 2009. The advantage of better educated customers is they are often willing to purchase premium products that have increased functional benefits.

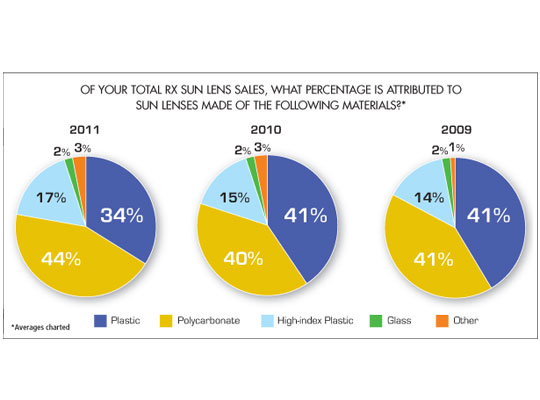

For example, premium lens materials are increasingly making significant contributions to the bottom line. Findings for the 2011 survey indicate polycarbonate lenses account for 44 percent of Rx sun sales, up from 40 percent in 2010. High-index plastic represents an additional 17 percent, up from 15 percent the previous year. Standard plastic (CR39) comprises 34 percent of market share. Five years ago in 2007 plastic led, accounting for 43 percent of Rx sun lens sales with polycarbonate trailing at 37 percent.

Customized Rx sun lens programs also contribute positively to profits. Of those surveyed, nearly half (48 percent) said they participate in prescription programs offered by name-brand sunwear/sport glass companies. These programs duplicate proprietary performance-oriented features in prescription lenses.

The performance factor brings up another aspect that should be beneficial to the sun business. The past several years have witnessed a merging between fashion-oriented and sport-oriented sunglasses. Fashion sunglasses, although designed for street and urban wear, often are available with a variety of premium performance features including polarization and grippable, rubberized bridges and temple tips. And manufacturers are dressing up sport glasses with hot colors and cool shapes without sacrificing performance. Surprisingly only 44 percent of the survey respondents said they believe the lines between fashion and sport sunwear are blurring, down from 50 percent in 2010. Of the 44 percent that feel the two categories are merging, 51 percent thought this is helping sales of both Rx and plano sunglasses. Only 6 percent felt the merging is hurting sunwear sales. Actually the blending of the two categories should be beneficial to both sunglass and sport glass sales. Those individuals—frequently women reluctant to wear sport glasses because in the past they often seemed bulky and unattractive—now have many fashionable options available to choose from. Performance features on the other hand appeal to those who may not be athletes, but think of themselves as having an active lifestyle. ECPs may need to point out these factors to their patients in their sunglass presentations.

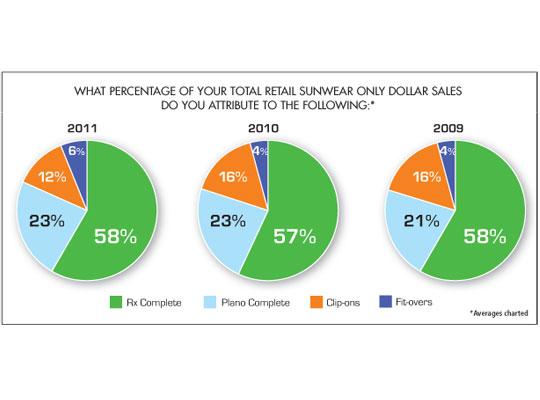

Another factor indicating positive news for the sunglass business is participants say Rx sunglasses accounted on average for 58 percent of total retail sunwear only dollar sales in 2011, significant because Rx products commanded the highest price points in the sunwear category. Also those polled reported 42 percent of their patients requested the plano sunwear they purchased be fitted with Rx sun lenses.

Additionally, although respondents said they dispensed clip-ons with only 13 percent of the Rx eyeglasses sold in 2011, representing 12 percent of retail sunwear dollars, clip-ons do contribute to the bottom line, selling for an average of $66.

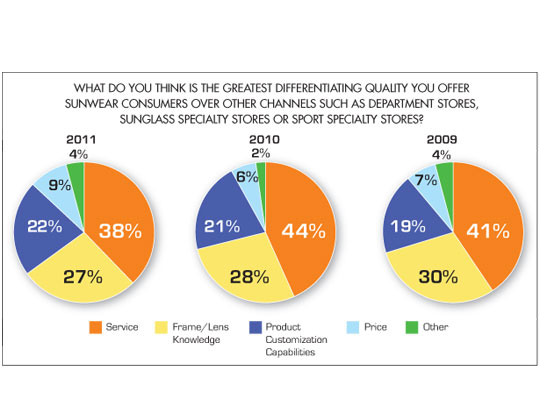

Also on the plus side, survey participants are well aware of the positive qualities differentiating them from other sunwear channels of distribution. Of the respondents, 38 percent cited superior service as the number one attribute setting them apart from the competition; followed by frame and lens knowledge, indicated by 27 percent; and product customization capabilities cited by 22 percent.

SCATTERED CLOUDS

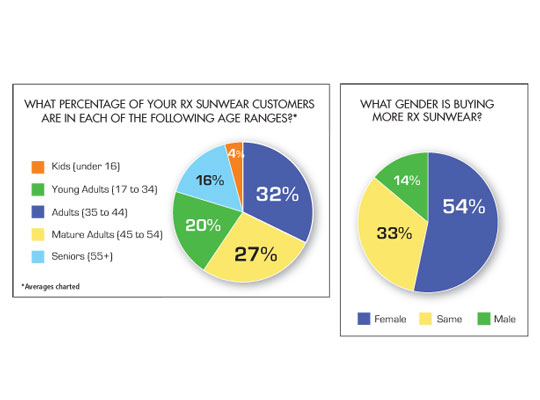

Despite warming trends in the sun business, there are clouds on the horizon and not necessarily the result of a struggling economy. ECPs need to continue reinforcing that everyone requires sun protection every day of the year. According to those surveyed, the largest percentage of their Rx sunwear customers (32 percent) were adults between the ages of 35 and 44, followed by mature adults 45 to 54 (27 percent). Young adults (17 to 34) represented 20 percent of the total and seniors (55 and older), 16 percent. Children under 16 accounted for only 4 percent of all Rx sunwear customers.

As for the gender buying more Rx sunwear, women were cited by 54 percent of the respondents as more likely to buy Rx sunwear. Only 14 percent said men bought more sunwear; 33 percent reported equal sun sales from both sexes.

In regard to selling sun year-round—although the sun knows no season—the majority of respondents characterized sunglass sales as high only during July and August (65 percent) and May and June (52 percent), and tumbling for the rest of the year, ranging from only 4 percent citing a high in January and February to 17 percent in September and October.

Another especially disturbing area in which optical is falling far short of its potential is in dispensing sunglasses to contact lens wearers. Just 54 percent of retailers surveyed claim they always recommend their contact lens patients buy sunglasses and 4 percent never suggest sunwear to these customers. Even more negative is the fact that only 15 percent said their patients make a sunwear purchase at the time they are fitted for new contact lenses, even though they will need sunglasses the moment they step outside. Certainly optical has an essential place in the sun. The sun has not lost any of its sizzle. The product is exciting and abundant. Just note all the dynamic styles featured in this issue. Every one of your customers, regardless of age or gender, needs sunwear. And they need it every day of the year. The challenge—and the opportunity—is yours. But you must be prepared to dedicate a significant portion of your practice, your environment and your attitude to sunglasses. You must be prepared to turn up the heat. ■

Methodology

20/20 Magazine’s 2011 Sunwear MarketPulse study is based on data collected from structured e-mail interviews with 214 independent optical retailers. The samples were derived from the proprietary Jobson Database.

All 2011 interviews were conducted in October 2011. Data is presented from a retailer or practitioner’s perspective and may reflect seasonal market and thus behavioral fluctuations.

All participants were contacted via e-mail invitation and offered an incentive of a chance to win a $200 American Express gift card.

This study was also conducted during the same time of year in 2007, 2008, 2009 and 2010. Trended data is charted wherever possible.

2010’s data was collected from structured interviews with 267 independent optical retailers, 2009’s data was collected from structured interviews with 159 independent optical retailers, 2008’s data was collected from structured e-mail interviews with 190 independent optical retailers and 2007’s data was collected from structured e-mail interviews with 180 independent optical retailers. All participants were contacted via e-mail invitation and offered an incentive of a chance to win a $200 American Express gift card each year from 2007 to 2010.

—Jennifer Zupnick

Senior Research Analyst

Jobson Optical Research