L&T’s 2012 Premium Lens MarketPulse Survey provides eyecare practitioners with a unique perspective on lens sales. The results of our annual study indicate how sales of spectacle lens designs, materials and treatments are trending among the 239 independent optical retailers across the country we polled. Use this valuable data to benchmark lens sales in your dispensary.

2012 Premium Lens MarketPulse Survey

2012 Premium Lens MarketPulse Survey

2012 Premium Lens MarketPulse Survey

2012 Premium Lens MarketPulse Survey

2012 Premium Lens MarketPulse Survey

2012 Premium Lens MarketPulse Survey

2012 Premium Lens MarketPulse Survey

2012 Premium Lens MarketPulse Survey

2012 Premium Lens MarketPulse Survey

2012 Premium Lens MarketPulse Survey

TOTAL SALES

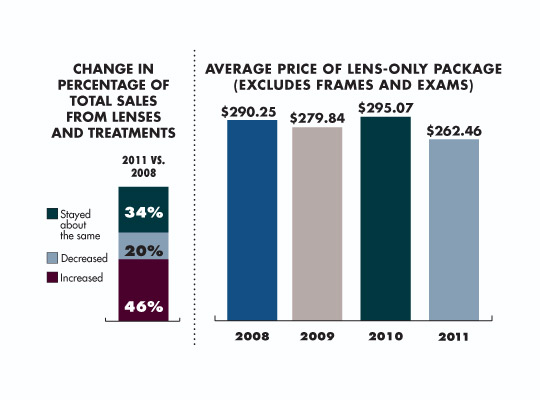

Compared to three years ago, 46 percent of retailers said that spectacle lenses and treatments made up a larger percentage of their location’s total gross dollar sales in 2011 compared to three years ago. This percentage had previously decreased steadily since 2008, but increased slightly this year. Fifty-two percent said pricing on spectacle lenses and treatments has increased compared to three years ago. Thirty-four percent said that Rx sun lenses as a percentage of total dollar sales increased over three years ago. Forty-two percent said pricing on premium sun lenses has increased over the last three years.

LENS SALES

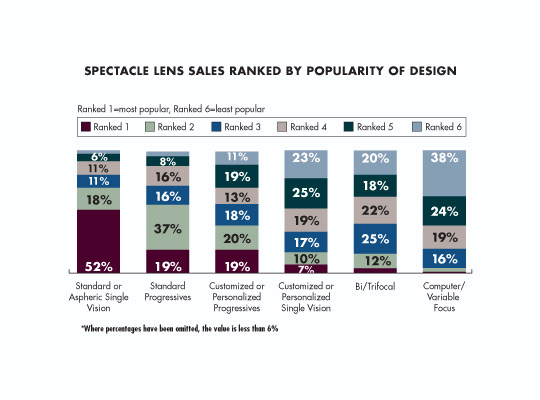

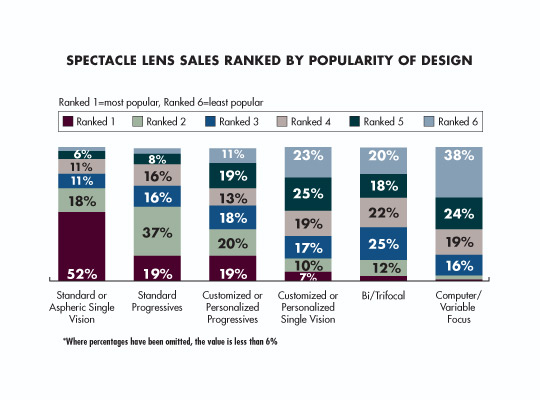

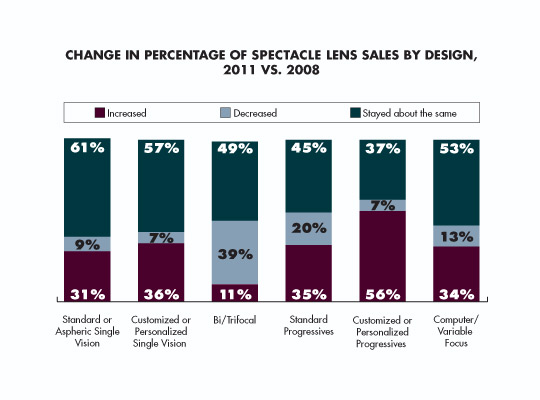

When asked to rank lens design by popularity, standard or aspheric single vision was ranked number one by 52 percent of retailers. Standard progressives and customized or personalized progressives were each ranked first by 19 percent. Fifty-four percent of retailers said short corridor lenses made up a moderate percent (11 to 49 percent) of their total progressive lens pair sales.

More than half (56 percent) of retailers said customized or personalized progressive lenses made up a greater proportion of their total lens sales in 2011 than they had versus three years ago. Comparatively, 35 percent said standard progressive sales had increased over the last year, while 39 percent said that sales of bifocals and trifocals had decreased as a percentage of total lens sales over the last year.

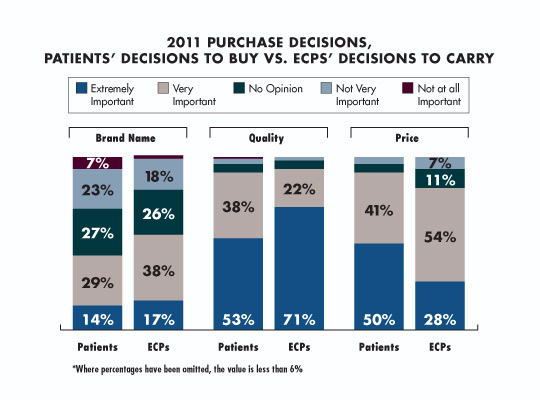

Fifty-five percent of retailers said brand name is very or extremely important to them regarding their decision as to which lenses to carry. Also, 93 percent of retailers said quality is extremely important to them regarding their decision as to which lenses to carry.

Sixty-four percent prefer lab brands over lab private labels.

Ninety-one percent of retailers said quality and price are very or extremely important to their patients regarding their decision as to which lenses to purchase.

PROGRESSIVES

Sixty-seven percent of retailers agree with the statement, “I promote the use of progressive lenses to all my presbyopic patients, including those who currently wear bifocals or trifocals.” This number is up from 48 percent last year.

When asked about familiarity regarding new progressive lens technologies, 88 percent of respondents were aware of the term “customized.” Eighty-one percent were aware of the terms “personalized” and “free-form,” and only 48 percent were aware of the term “contrast enhancing.”

Eighty-six percent of respondents said they are very or extremely satisfied with the personalized progressive lenses they dispense.

COMPUTER/OFFICE LENSES

Most retailers surveyed (65 percent) said that computer/office lenses make up an insignificant percentage (10 percent or less) of their total lens pair sales.

LENS MATERIALS

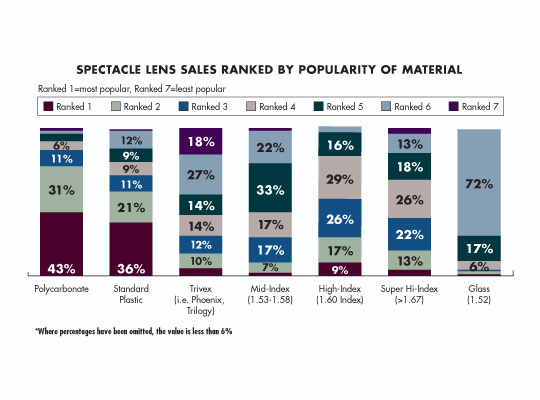

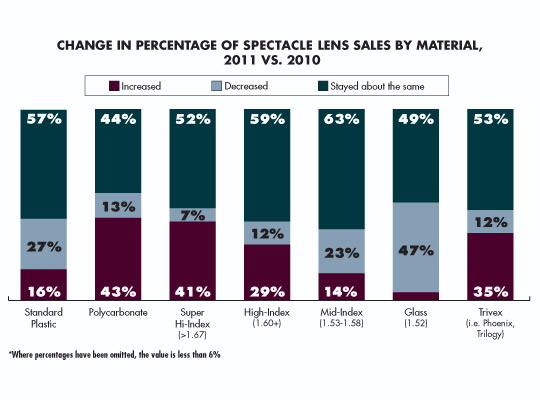

When asked to rank lens material by popularity, polycarbonate was ranked first by 43 percent of the retailers. Standard plastic was ranked first by 37 percent. Glass was ranked least popular by the most retailers (72 percent).

Forty-three percent of retailers said that their 2011 polycarbonate lens sales increased as a proportion of total lens pair sales compared to 2010. Forty-one percent said their sales of super high-index lenses had grown since 2010, and 35 percent said Trivex sales had increased over the last year.

Sixty-three percent said their mid-index lens sales had stayed flat. Glass was the worst performer, with 47 percent saying glass made up a smaller proportion of their total lens sales in 2011 than in 2010.

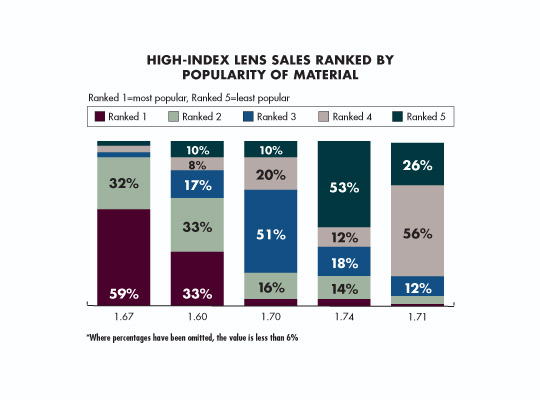

HIGH-INDEX LENSES

When asked to rank high-index lenses based on popularity, 59 percent ranked 1.67 as most popular and 33 percent ranked 1.60 as most popular. Comparatively, 1.74 was ranked least popular by 53 percent of retailers.

LENS TREATMENTS

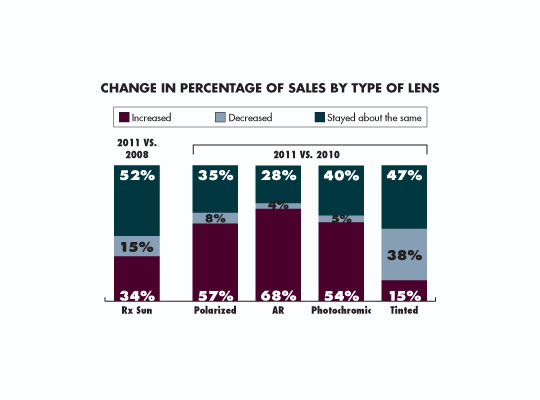

An impressive 68 percent of retailers surveyed said they had experienced an increase in AR lens sales as a proportion of total lens sales in 2011 versus 2010. Fifty-seven percent saw an increase in polarized lenses and 54 percent saw an increase in photochromic sales over the same period.

For 38 percent of retailers surveyed, tinted lens sales stayed about the same versus the year before.

Seventy-five percent of retailers said they offer two different price points for AR lenses—one being standard, the other being premium.

IMPACT OF REFRACTIVE SURGERY

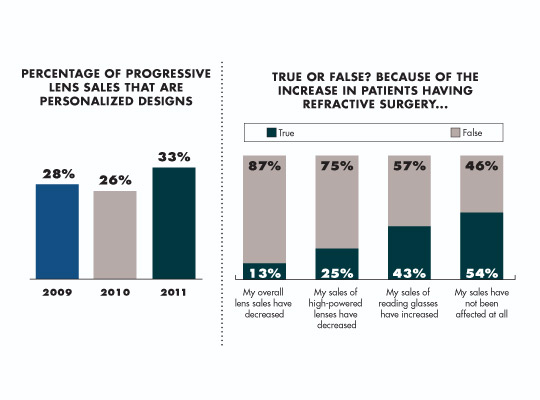

Forty-three percent of retailers agree that because of the increase in patients having refractive surgery their sales of reading glasses have increased, while 25 percent say specifically high-powered lens sales have decreased. Fifty-four percent, however, say sales have not been affected at all.

READING GLASSES

For some retailers (44 percent), reading glass unit sales stayed about the same in 2011 compared to three years ago. Thirty-seven percent of respondents experienced an increase in reader sales over this time period. Among those who sell readers, 34 percent said their OTC/ready-made reader sales had increased in 2011 and custom-made reader sales increased for 37 percent of respondents at locations that sell readers.

LENS PACKAGES

Forty-eight percent of retailers say they use lens-only package pricing. The average price of this lens-only package is $262.46.

OUTDOOR EYEWEAR

Forty-four percent said they have increased discussions with their patients on the importance of UV and HEV absorbing eyewear for outdoor use and 33 percent have actually written more Rxs for them in the last three years.

Forty-eight percent said they have increased discussions with their patients on the importance of children’s outdoor eyewear/sunwear and 34 percent have actually written more Rxs for them in the last three years. ■

Methodology

This sample was derived from the proprietary Jobson Optical Research database. This survey was conducted by Jobson Optical Research's in-house research staff. Data collection was conducted in February and March 2012. Only the responses of independent optical retailers who dispense premium lenses are included in the report. The sample consists of 239 independent optical retailers. All participants were recruited by e-mail and the questionnaire was completed via the Internet. Four years of data is provided for comparisons where possible.

![]() —Jennifer Zupnick

—Jennifer Zupnick

Senior Research Analyst

Jobson Optical Research